The financial sector of the U.S. economy has had nearly a year to address the problems that exacerbated the crisis last fall. But many observers think that the banks haven’t done enough, and that another round of trouble may be developing for the sector. I will outline some of those concerns and then suggest some ways to use options to profit if there is indeed another shoe to drop in banking.

The Thesis

The primary obstacle facing large banks is that they still carry most of the “toxic assets” that caused them so much trouble last year. As Elizabeth Warren explained recently, changes to accounting rules allowed banks to appear solvent only by allowing them to continue to obscure the market value of their troubled assets. By allowing banks to continue operating without any transparency or accountability, the federal government bought the banking industry some time, but did not address the fundamental problem. While some banks have begun quietly unloading some of their non-performing mortgages at steep discounts, they cannot do so in any real size without risking large write-downs that would spook equity holders.

A robust economic recovery – especially one in which new high-paying jobs are created and consumers regain their confidence – would lift the real estate market and boost the values of troubled assets. But while the administration and the banks have further leveraged themselves on the hope that such a recovery is forthcoming, there is little reason to expect a sustained rebound. Even if we do see improvements beyond the round of cost-cutting that enabled still-paltry, if positive second quarter earnings reports, such a recovery is likely to be a “jobless” one that will be insufficient to improve the fortunes of the major banks.

Two other catalysts to watch for include the commercial real estate (CRE) market and increased predatory activity on the part of banks themselves. The CRE story has been covered in great detail and has attracted widespread attention, mostly, I think, because it would amount to a new problem scenario in addition to all the familiar problems. The federal TALF program was extended by three to six months on August 17th and is intended to facilitate purchases of commercial mortgage-backed securities, but it is unclear whether government support will be sufficient to inspire continuing weak demand.

More alarming are the new products launched by major banks like Morgan Stanley (MS), JPMorgan Chase (JPM), Citigroup (C), and Wells Fargo (WFC). According to a recent story in BusinessWeek, these institutions are now getting into the sleazy payday loan business, are offering commercial loans linked to credit-default swaps (essentially increasing the financing burden on businesses precisely when they are least able to afford it), and are now approaching retail customers with structured notes – derivative instruments with complicated terms and opaque risks. Some or all of these might boost revenues at the banks over the short-term, while also entangling consumers and banks alike in a new round of ill-advised risk-taking.

In short, the fundamental picture for the major U.S. banks doesn’t look very different now than it did several months ago, especially once we discount the temporary effects of accounting changes and short-term stimulus packages. Bank stocks seem priced for a major economic recovery, but a quarter or two of continued weakness or negative surprises from the two other catalysts we mentioned could spark a substantial selloff in bank stocks.

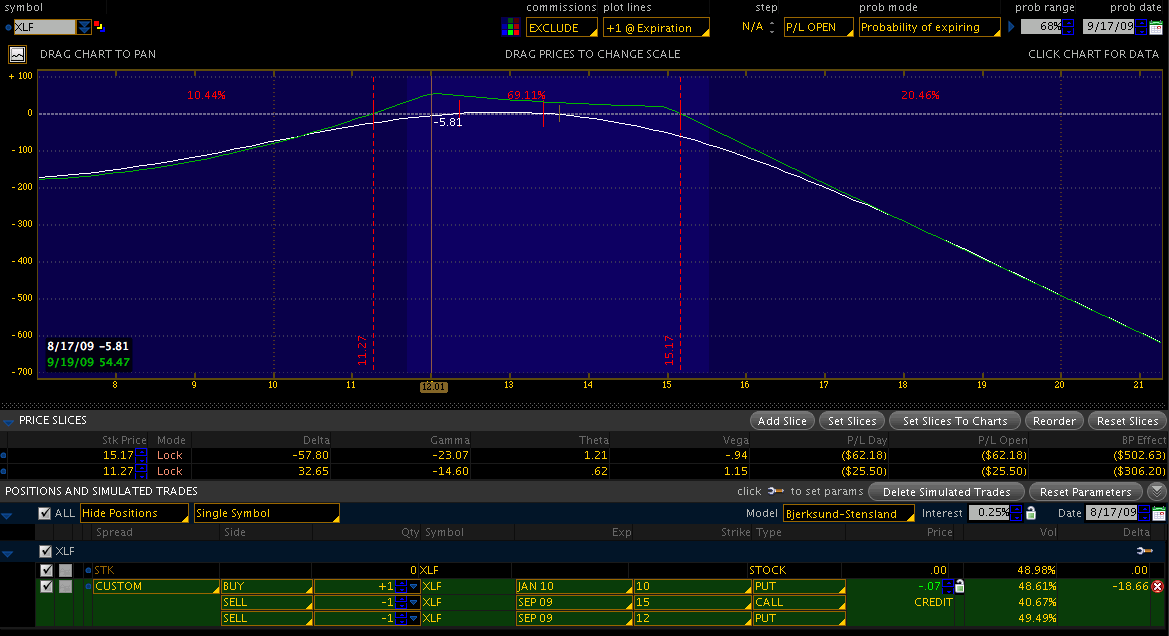

The Trade

Options are a valuable tool for expressing views that can’t be stated in any other way. For simple buy/sell theses, buying or shorting a stock or ETF is sufficient. But in this case, we want to take a more nuanced position. It’s entirely possible, even if unlikely, that the U.S. economy will rebound strongly and bank stocks will rise amidst a new bull market. It’s also possible that no major surprises will emerge and the banks will be range-bound for months to come. So a straightforward put purchase isn’t the most desirable way to make this play.

We want a position that is long vega – meaning that it will profit from an increase in implied volatility – since a decline in the financial sector is more likely than not to be a relatively sudden affair. We also want a position with some positive theta: since it may take some time for this pessimistic thesis to play out, we want to profit from time decay rather than let the value of our position trickle away. Finally, we want a position with some negative delta: we are bearish on the sector, after all.

click to enlarge

The XLF January 2010 10 puts could recently be bought for about $0.32; with -0.13 delta and 0.2 vega, these puts satisfy the first and third requirements. The XLF September 12 puts could recently be sold for about $0.20, and the September 15 calls could recently be sold for about $0.18. By selling this front-month strangle, we can bring in some income to help defray the cost of those back-month puts. The resulting three-legged position can be opened for a net credit of about $0.07; it will be profitable at September expiration if XLF is anywhere between roughly $11 and $15, with a maximum profit point near $12. At current levels of implied volatility, there is about a 70% chance that this position will be profitable at September expiration.

No trade is complete without a serious consideration of the risks involved. Because the front-month strangle we’re selling is only partially hedged (the long January put covers our short September put), it faces unlimited risk on the call side. As a result, it is advisable to hedge any upside breakout above $15 with either stock or long calls. We follow a version of this approach in our newsletter, and Condor Options' members have witnessed how helpful even a weekly rebalancing hedge can be.

Managing the trade after September expiry is relatively straightforward: as long as the underlying thesis of the trade is intact, we can sell short-term options against our core long position to generate income and reduce our cost basis. If the financial sector does begin to weaken, it will make sense to look further out of the money in order to allow more room for price declines.